New Global Macro Evidence and Forecast Update

New Global Macro Evidence and Forecast Update

"Each [failed forecast] involved historical discontinuity, and, in the early stages…unlikely outcomes. The basic problem was…situations in which trend continuity and precedent were of marginal, if not counterproductive value." – 1983 CIA Study of Significant Historical Forecasting Failures

New Evidence This Week

National Security

In two stories, very senior US Government officials have warned that China has speeded up its plans for attacking Taiwan. The BBC reported that, “China is pursuing unification with Taiwan on a much faster timeline than previously expected…Beijing has decided the status quo is no longer acceptable”, US Secretary of State Antony Blinken said at an event at Stanford University. The Financial Times reported that “The head of the US Navy has warned that the American military must be prepared for the possibility of a Chinese invasion of Taiwan before 2024, as Washington grows increasingly alarmed about the threat to the island. Admiral Mike Gilday, chief of naval operations, said the US had to consider that China could take action against Taiwan much sooner than even the more pessimistic warnings…Underscoring the mounting concern about Chinese military activity near Taiwan, which has increased in the wake of US House Speaker Nancy Pelosi’s visit to Taipei in August, Joe Biden has on four occasions as president warned China that the US would intervene to defend Taiwan from an unprovoked attack.”

In a new column, AEI’s Chris Miller concluded that, “The ‘Silicon Shield’ Won’t Protect Taiwan from a Chinese Invasion.” He notes that, “All the technology we take for granted is ultimately about the silicon chips on which all of the actual computing takes place. But also, military power has over the past half century increasingly depended on the ability to apply computing to military systems. Very few people realize that a pretty small industry with a really small number of companies has defined military power and is defining the nature of U.S.-China competition today. Both countries realize that the computing that chips have made and will make possible over the coming decade will be foundational to economic influence and prosperity – but also to all future weapons systems…

“The military balance in the Taiwan Straits and the Asia-Pacific region has dramatically shifted toward China over the past decade and will keep shifting in this direction. But the U.S. cannot compete with China in terms of ships and airplanes and missiles produced. We can’t rely on quantity, but instead on quality. The differentiation factor needs to be a mix of sensing, of computing, networking on the battlefield.

“The U.S. government’s bet is that if we can make sure that most of the production of chips and transistors happens offshore of China, and we control what types of chips go into China, we can make sure that the U.S. has a really meaningful advantage in harnessing computing power for military, intelligence and cybersecurity systems. Over the next 10 years, as we get a doubling in computing power per square inch of silicon every two years, that will be a meaningful difference – if we’re able to keep the existing controls in place and if China is not able to catch up. It seems like the only possible strategy for halting the decline in the military balance, since U.S. defense spending won’t double.”

Miller was asked, if “the fact that TSMC is the global leader in producing computer chips make it more or less likely that there will be an armed conflict over Taiwan?”

His answer was deeply sobering: “I think it makes it more likely. The Taiwanese government argues that Taiwan benefits from the ‘Silicon Shield’ – meaning that it is so important for the global economy that China won’t attack it because it will be very costly for Beijing. The presumption that interdependence will protect us from war has been tested this year in Ukraine. It sounds like Merkel’s energy policy, which didn’t work out very well. I think the opposite is true – that the global economy’s and the U.S. economy’s reliance on chips from Taiwan emboldens China to attack, by making China think that the U.S. is less likely to come to Taiwan’s aid.”

It is in this context that The Heritage Foundation’s new 2023 Index of Military Strength is so worrying. “It is therefore critical that the American people understand the condition of the United States military with respect to America’s vital national security interests, threats to those interests, and the context within which the U.S. might have to use “hard power” to protect those interests…As currently postured, the U.S. military is at growing risk of not being able to meet the demands of defending America’s vital national interests. It is rated as weak relative to the force needed to defend national interests on a global stage against actual challenges in the world as it is rather than as we wish it were. This is the logical consequence of years of sustained use, underfunding, poorly defined priorities, wildly shifting security policies, exceedingly poor discipline in program execution, and a profound lack of seriousness across the national security establishment even as threats to U.S. interests have surged.”

This is consistent with reports from various wargames that a conflict between the United States and China over Taiwan would be intense and bloody, with a substantial chance that the United States would either lose or win at a very high cost. This is almost certainly an outcome whose implications most people – including very sophisticated investors – have not yet fully considered (note that we have, as we’ve repeatedly described in our Regime Forecasts, available to paid subscribers of The Index Investor).

The Special Competitive Studies Project released its Defense Panel Interim Report. It was not uplifting. “The character of war is changing. Before the end of this decade, the United States and its allies will face a new kind of warfare. The emergence of new, advanced technologies – including artificial intelligence – combined with operational concepts that harness them in innovative and unexpected ways, are creating new ways to apply military force. America’s principal rival, China, is determined to harness these changes with the aim of eroding or even leapfrogging the United States’ military strengths.

“Meanwhile, the brittleness of America’s defense industrial base, the slow transition in U.S. military capabilities from a small number of exquisite legacy systems to many lower-cost systems, and the struggle to shift from traditional operational concepts compound these challenges and risk strategic exposure for the United States. The stakes could not be higher. If the United States does not rise to this challenge, the consequences could be dire: a shift in the balance of power globally, and a direct threat to the peace and stability that the United States has underwritten for nearly 80 years in the Indo-Pacific – the most economically, technologically, and resource-critical region of this century.”

The Economy

The recent economic and political gyrations that have roiled the UK are another indicator that our current High Inflation Regime carries with it risks that many haven’t seen before, unless, as they say in polite company, you are “of a certain age”. Let’s start with two observations. First, the Truss government proposed to cap energy prices, rather than protecting people and businesses by subsidizing high energy costs. Not letting prices rise was a clear disincentive to innovation and greater investments in energy supply. Second, the proposal to sharply cut top tax rates in a bid to increase the UK’s rate of growth (a very important goal) ran smack into concerns about the likely success of the policy itself (as trickle down doesn’t have a great track record) and rising UK government debt. The result was a bond market crisis that was made worse by the consequences of rising interest rates on pension funds’ use of a leveraged approach to liability driven investing (as the FT’s Robin Wigglesworth wrote, "In finance there is nothing quite so dangerous as a supposedly safe strategy”).

In the United States, high energy prices have contributed to rising inflation, a slowdown in consumer spending, and a change in the political winds that may deliver the House of Representatives (and, far less likely, the Senate) to a Republican majority, which will very likely lead to two years of policy stasis at a time when will likely be increasingly dangerous. The obvious way to reduce energy prices is to increase oil and gas production – but as Chevron’s CEO noted last week, environmental restrictions on the construction of new pipelines, storage, and export facilities has limited that option (as has the desire of private equity fund and other investors to finally realize a positive return on a decade of investment in fracked wells).

And so the Federal Reserve is left with the task of raising rates to reduce inflation, which brings with it a serious risk not just of more bankruptcies in the highly leveraged corporate sector, but also increasing concerns about the US government deficit, as higher rates will lower asset prices and reduce tax revenues from capital gains while also increasing interest costs further increasing the size of a federal deficit that will already be growing because of the increase in both military spending and automatic countercyclical stabilizers in a weakening economy (e.g., food stamps and Medicaid). To top off this increasingly fraught situation, multiple indicators are showing a sharp decline in liquidity in the market for US Government bonds, which will only worsen the impact if “something” happens – which will very likely take us by surprise, because in complex adaptive systems relationships between cause and effect are often time delayed and very non-linear.

In sum, recent events in the UK have painfully shown that today there are a lot of things that can go suddenly and violently wrong in the global economy and financial markets, whose complexity shows every sign of having outrun current policymakers’ ability to understand and effectively influence them. As we have said for a long time in The Index Investor, we are living in a period that is far more dangerous than many appreciate.

Social

In Misperceiving Economic Success, Fehr and Vollmann observe that, “although the meritocratic ideal is appealing for fairness and aspirational reasons, there is a growing concern that a belief in meritocracy reinforces pre-existing inequality. Therefore, it is important for society and policy measures to understand how meritocratic beliefs are formed and contribute to income disparities.” They show how “meritocratic beliefs are often invoked as justification of inequality… and are shaped by economic status.” They also show how they contribute to the moral justification of inequality: “Success causes a change in beliefs about success depending on effort rather than luck, [and] beliefs affect how much inequality people accept. Successful people prefer to remain ignorant about the true underlying reasons for their success. And there is no evidence that these beliefs are moderated by political orientation.”

As noted in the next section, this insensitivity has been an important driver of the widening gap between the elite and the masses in the United States.

Politics

The recent events in the UK also highlight a critically important political trend that has arguably been underway since the 2008 Great Recession or longer. Let’s start with this chart from the Financial Times, which describes different voter groups’ positioning on social and economic issues, as well as changes in the Labor and Conservative parties’ policy positions over the past three years.

Perhaps the most interesting point to note is the absence of most conservative voters from the upper right quadrant – the home of traditional “Shire” Tories, who held conservative economic and social positions. In the 2019 general election, Boris Johnson moved the party towards the upper left quadrant, maintaining relatively conservative social positions but taking more liberal positions in economic issues. This strategy “broke the Red Wall” in Northern England, where the Conservatives won parliamentary seats that Labor had held for years.

The chart also shows how Liz Truss’s recent policy proposals attempted to take the Conservative Party back into the top right quadrant. That worked under Margaret Thatcher, but failed disastrously this month.

The critical point is this: That changes in technology have begotten changes in the economy and society that have caused many voters views to migrate towards the upper left quadrant – still relatively conservative on social issues, but more liberal on economic issues and the need for government to push back on the forces driving increased in inequality and making it far harder to sustain a traditional “middle class” lifestyle (e.g., good health care, housing, higher education for one’s children, job and retirement security, etc.).

In the United States, polling data show that while the same forces are at work, our political parties have been slower to react to them. Specifically, the Democratic Party is still relatively more liberal on both social and economic issues, while the Republican Party is relatively more conservative on them. As Martin Gurri, Joel Kotkin, Ruy Texiera, Matt Goodwin, Brink Lindsey and other analysts have noted, party differences are increasingly less consequential than the split that has emerged between the elites and the mass. The former tend towards Libertarian beliefs (conservative on economics and liberal on social issues), while the latter have moved toward the quadrant that Boris Johnson sought to move the Tories: Conservative on social issues, but liberal on economic ones. One of the reasons this change has been so hard to recognize is our lack of a common term to describe this quadrant.

In one of the earliest analyses to identify it (Lilie and Maddox’s 1981 classic paper An Alternative Analysis of Mass Belief Systems: Liberal, Conservative, Populist, and Libertarian, they called these voters “Populists”. However, because that term has been used in different ways over the years, it never really caught on to describe a growing group of voters.

This month, Tyler Cowen wrote a very thoughtful post on this trend on his website, MarginalRevolution.

“The main difference between Classical Liberals and the New Right…is how much faith each group puts in the possibility of trustworthy, well-functioning elites.

“A common version of the standard classical liberal view stresses the benefits of capitalism, democracy, civil liberties, free trade (with national security exceptions), and a generally cosmopolitan outlook, which in turn brings sympathy for immigration. The role of government is to provide basic public goods, such as national defense, a non-exorbitant safety net, and protection against pandemics.

“In the classical liberal view, elites usually fall short of what we would like. They end up captured by some mix of special interest groups and poorly informed voters. There is thus a certain disillusionment with democratic government, while recognizing it is the best of available alternatives and far superior to autocracy for basic civil liberties…

“The New Right thinkers are far more skeptical of elites. They are more likely to see elites as evil and pernicious, and sometimes they (implicitly) see these evil elites as competent enough to actually wreck society. The classical liberals see checks and balances as strong enough to limit the worst outcomes, whereas the New Right sees ideological conformity and indeed collusion within the Establishment. Checks and balances are a paper tiger…Free trade becomes seen as a line peddled by the elite, and that is an elite unconcerned with the social and national security costs of a deindustrialized America. Globalization more generally becomes a failed project of the previous elite.”

In essence, and as we saw in the 2016 and 2020 presidential elections, the most important fault line in American politics today is no longer between the Democratic and Republican Parties, but between a Libertarian elite and a Populist mass.

In the UK, Boris Johnson grasped this and tried to move the Tory party towards the Populist quadrant. The great tragedy is that his political success was undermined not only by his personal failings, but also by the inability or unwillingness of his parliamentary majority to follow through with policies that were consistent with this new political positioning. I could also argue that Donald Trump’s attempt to move the Republican Party in the same direction met the same fate. But this is not to say that future leaders in the UK and US won’t have more success.

Unfortunately, in the US we’re not close to that. Instead, we have the fundamental elite/populist conflict awkwardly playing out (and people trying to understand it) using the traditional – and outmoded – Democrat/Republican framework.

A greater concern, as Martin Gurri has noted, is that in our densely interconnected social media culture, the popular masses know what they are angry about and what they are against. But they don’t know what they’re for – and today’s elite seems wither unwilling or unable to address their core problems (e.g., quality, affordable healthcare, high quality, low cost education for their children, rising real compensation and a reasonable degree of job security, affordable housing, a secure retirement, and what they perceive as elite’s condescension towards them).

The great uncertainty is the extent to which this widening and increasingly hostile gulf between our elites and the masses will limit the United States’ ability to mount and sustain over time an extremely expensive (in all senses) but ultimately successful collective response to a future existential threat like a war between Russia and NATO, a war with China over Taiwan, or a deep and extended recession.

You can improve your own ability to anticipate, accurately assess, and adapt in time to emerging threats by taking our eleven module course at The Strategic Risk Institute. It costs only $250, and leads to a certificate in Strategic Risk Management and Governance.

Background

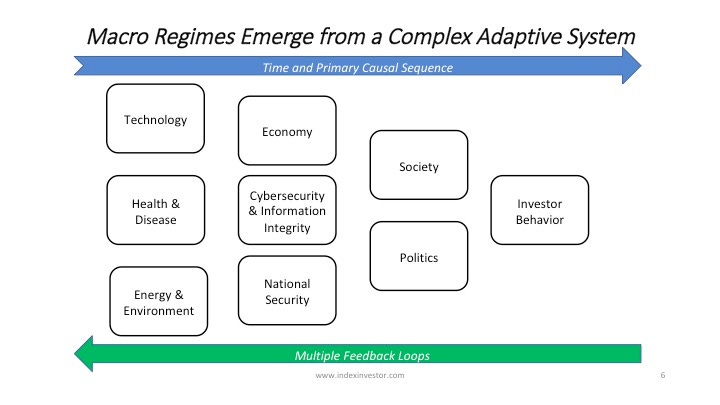

At the Index Investor and Retired Investor, our information collection, analysis, and forecasting process is based on this model of how developments in different issue areas interact in a rough chronological sequence (albeit in a complex manner) to produce different global macro regimes (which we label Normal Times, High Uncertainty, High Inflation, and Persistent Deflation).

In each of these areas we continuously seek new evidence, which classify as significant and highly valuable if either (1) it is an “indicator”, which reduces our uncertainty about the value of a parameter in our mental model for making sense of the dynamic macro system, or (2) it is a “surprise” which increases our uncertainty about either the range of potential values for a parameter or the structure of our model.

Each week in this newsletter we review high value new evidence and its significance in some or all of these areas. Each quarter we summarize these weekly newsletters in new issues of The Index Investor and Retired Investor, as well as updated 12 and 36-month global macro regime probabilities and any changes to our model portfolios.

The Neutral portfolio places 10% weights on nine major asset classes, and 5% each to two active strategies (Equity Market Neutral and Global Macro), which should have low correlations with returns on major asset classes.

The Systematic portfolio changes asset class weights based on the extent of our estimate of their respective degrees of over or undervaluation. This portfolio expands the fixed income asset class to include possible allocations to Investment Grade and High Yield credit products. Allocations to Equity Market Neutral and Global Macro remain constant at 5% each. Finally, when some asset classes are so overvalued that they have a zero weight, but other asset classes are not sufficiently undervalued to absorb reallocations away from the overvalued classes, the excess cash is placed in a mix of Cash (short term Treasury Bills and Notes) and Gold.

The Subjective portfolio is our attempt to outperform the Neutral and Systematic portfolios via active management. More often than not, it underperforms the Systematic portfolio, proving that we find successful active management over the long term just as challenging as everyone else.

Model Portfolio Performance

In the second quarter of 2022, as high valuations retreated across multiple asset classes, the Neutral portfolio was down (10.1%) from the end of March, the Systematic portfolio was down (8.1%), and the Subjective portfolio was down (8.0%). By comparison, a Traditional portfolio of 60% US Equity and 40% US Government Bonds was down (11.4%).

For the first half of 2022, the Neutral portfolio was down (8.0%) from 31 December 2021, the Systematic portfolio was down (4.9%), and the Subjective portfolio was down (5.0%). By comparison, a Traditional portfolio of 60% US Equity and 40% US Government Bonds was down (8.7%).