New Global Macro Evidence and Forecasts

New Global Macro Evidence and Forecasts

New Evidence This Week

Energy and the Environment

In China’s Growing Water Crisis, Collins and Reddy conclude that, “China is on the brink of a water catastrophe. A multiyear drought could push the country into an outright water crisis. Such an outcome would not only have a significant effect on China’s grain and electricity production; it could also induce global food and industrial materials shortages on a far greater scale than those wrought by the COVID-19 pandemic and the war in Ukraine. Given the country’s overriding importance to the global economy, potential water-driven disruptions beginning in China would rapidly reverberate through food, energy, and materials markets around the world and create economic and political turbulence for years to come.”

In Methane Hunters: What Explains The Surge In The Potent Greenhouse Gas? Hook and Campbell from the Financial Times write that, “About 15 years ago, its researchers observed an uptick in atmospheric methane, a potent greenhouse gas with a warming impact 80 times greater than CO2. Many researchers initially assumed the increase was linked to fossil fuel production. Methane is the primary ingredient in natural gas but is also produced by other human activities such as landfills, rice paddies and raising cattle. In the past few years, however, that uptick has accelerated into a surge. The implications for global warming are immense: of the 1.1C increase in global temperatures since pre-industrial times, about a third can be attributed to methane. Atmospheric methane had its highest growth rate ever recorded by modern instruments in 2020, and then that record was broken again in 2021. Nobody knows exactly why…

“One thing they have begun to identify is what kind of methane is culpable for the increase. Methane derived from fossil sources contains more of the carbon-13 isotope than atmospheric methane, while that produced by microbial sources — such as wetlands, cattle and landfills — contains less. Since the beginning of the industrial revolution, fossil fuel emissions have tilted the ratio of methane isotopes in the atmosphere towards carbon-13. But around 2007, when atmospheric methane started to climb again, that isotopic ratio went into reverse. The recent increase in methane is not coming primarily from fossil fuels, but from other sources.

“That suggests the planet itself could be emitting more methane, and it is not slowing down… Something significant has happened… Unravelling the mystery will reveal whether or not the world might face the worst-case scenario of a “methane bomb” — a feedback loop where a warmer planet emits more of the gas naturally, driving temperatures up further. It’s a terrifying prospect, one that scientists studying this topic tend to tiptoe around, particularly in interviews.”

Over the years, in The Index Investor and Retired Investor, we have emphasized the substantial irreducible uncertainty inherent in all climate models, and thus their potential for missing critical tipping points with non-linear negative consequences. This is may be a perfect example of that risk. Rapidly rising methane emissions is potentially a very dangerous emerging threat, with major implications across multiple domains. We should all continue to carefully monitor it.

National Security

In China Hasn’t Reached the Peak of Its Power, AEI’s Oriana Skylar Mastro and Derek Scissors write that, “As relations between the United States and China have spiraled down to a half-century low, a frightening new narrative has taken hold among some U.S. analysts and policymakers. It supposes that China’s window of opportunity to “reunify” Taiwan with the mainland—one of Chinese President Xi Jinping’s core foreign policy objectives—is closing rapidly, intensifying the pressure on Beijing to act swiftly and forcefully while it still has the chance.

“This narrative rests on the belief that China’s rise is nearing its end. Unprecedented demographic decline, a heavy debt burden, uneven innovation, and other serious economic problems have slowed China’s growth and are likely to slow it even further, leaving the country without the military power or political influence to challenge the United States. Beijing is aware of these headwinds, the thinking goes, and is therefore likely to act soon, before it is too late. As the scholars Hal Brands and Michael Beckley [also from AEI] have argued, ‘China is tracing an arc that often ends in tragedy: a dizzying rise followed by the specter of a hard fall.’ In their view, it is now or never if China wants to redraw the world map.

“But such analysis is misguided. True, China’s economic ascent has slowed and will eventually reverse, impeding Beijing’s military and political aspirations. But a “hard fall” is not in the cards. Any decline from China’s economic peak is likely to be gradual—and possibly eased by heavy spending on research and development explicitly aimed at partially off setting the country’s demographic and debt-related woes. In fact, current income and defense spending trajectories suggest that China will have more resources to compete militarily with the United States over the next ten years than it has had over the last 20. As a result, Beijing will become more—not less—capable of projecting power while the United States will have difficulty countering Chinese military challenges in Asia. Far from a narrow window to achieve their geopolitical ambitions, then, China’s leaders have space to bide their time.”

Bottom Line: The timing of a potential Chinese invasion of Taiwan remains a critical uncertainty. But in the meantime, the possibility of an accident that triggers rapid conflict escalation on unfavorable terms for the United States and its allies will continue to be a dangerous threat.

Society

In Rent Forever and Love It, Joel Kotkin warns that, “the globalized commodification of housing will destroy democracy… After the Second World War, wider home ownership created unprecedented middle-class stability, broad social benefits, and helped subsidize comfortable retirements. Democracy grew stronger with the growth of a stable middle rank with a natural stake in economic progress and an interest in the political system… After 1940, U.S. homeownership rates grew rapidly, from 44 percent to 63 percent thirty years later. Now, the trend is in the opposite direction. Millennials are less likely to be homeowners than baby boomers and Gen Xers. The homeownership rate among millennials ages 25 to 34 is 8 percentage points lower than baby boomers and 8.4 percentage points lower than Gen Xers in the same age group. Their chances of buying now have been made more problematic by the rapid rise in interest rates…

“On both sides of the Atlantic, large financial institutions like Britain’s Lloyds Bank and BlackRock have placed multi-billion dollar bets on buying homes for the rental market. In the first quarter of 2021, investors accounted for roughly one out of every seven homes bought, a marked increase from previous years. The popular notion is of a “rentership” society where people remain renters for life…It might assure a steady profit for the landlord class, but would destroy the dream of ownership for the average person.”

Kotkin’s analysis is important, in so far as you believe (as we do) that a key cause of social and political anger (and hence the attraction of political extremes) is the extent to which the post-World War 2 trappings of a middle class existence are out of reach for a rapidly growing number of people who had been raised to expect them. These include owning a home, secure health insurance, a reasonable measure of job security and rising real pay, a secure retirement, and being able to send your children to college. Taken together, they constitute the wicked problem facing leaders today.

In sum, while as investors we appreciate the transformation of single family housing into an investable asset class, we also recognize that, beyond an uncertain threshold this process could significantly worsen social and political conflicts.

Noah Smith is an incisive social and political observer whose analysis I greatly admire. He recently wrote a long piece on The Elite Overproduction Hypothesis that Peter Turchin has argued is a key driver of social and political unrest. Looking at developments over the past twenty years in the United States, Smith finds it compelling. More importantly, this appears to be a problem that isn’t going to go away anytime soon. Well worth a read.

Politics

In The Accelerating Threat of Political Assassination, Hoffman and Ware say out loud something that has been increasingly troubling people (like me) who great up in the 1960s, and remember the assignations of Malcolm X and Martin Luther King and John and Robert Kennedy, as well as the attempted assassination of George Wallace – and what followed: “We may be entering a similarly dangerous period in the United States, where elected or appointed officials and political candidates face a heightened risk.”

“Today’s growing wave of assassination attempts has crossed ideologies. Certain adherents of the far left have been responsible for attempts on the Republican baseball practice and more recently Justice Kavanaugh. But the far-right is also active in this space and was responsible for the most recent successful high-level political assassination in the country: the killing of Reverend Clement Pinckney, state senator of South Carolina, at the Mother Emanuel AME Church in Charleston in 2015. Jihadists often place prominent figures in their crosshairs, as demonstrated by a recently disrupted plot against George W. Bush. Even the more nascent male supremacist movement has its targets: A so-called “men’s rights activist” attacked the home of U.S. District Court Judge Esther Salas in July 2020,killing her son. The emerging trend is due in no small part to the reemergence of so-called ‘accelerationism’ as a distinct violent extremist strategy. For extremists seeking to sow chaos and speed up some cataclysmic societal collapse, high-profile politicians provide an attractive target, as symbols of the mainstream liberal political order.”

Given the extent of social anger and political polarization in the United States today, the extent and severity of the consequences that would follow one or more high profile political assassinations are a critical uncertainty.

You can improve your own ability to anticipate, accurately assess, and adapt in time to emerging threats by taking our 11 module course at The Strategic Risk Institute. It costs only $250, and leads to a certificate in Strategic Risk Management and Governance.

Background

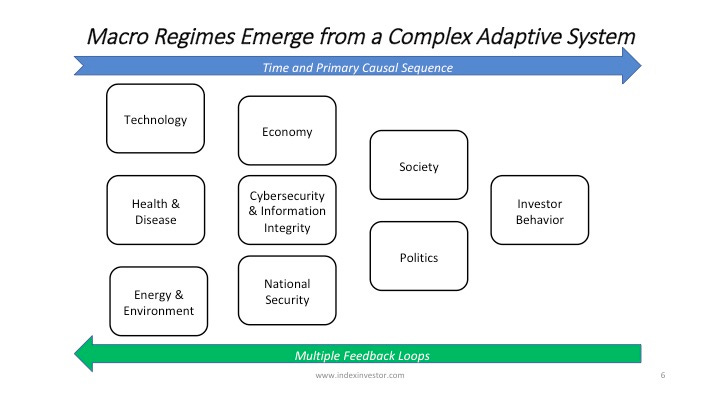

At the Index Investor and Retired Investor, our information collection, analysis, and forecasting process is based on this model of how developments in different issue areas interact in a rough chronological sequence (albeit in a complex manner) to produce different global macro regimes (which we label Normal Times, High Uncertainty, High Inflation, and Persistent Deflation).

In each of these areas we continuously seek new evidence, which classify as significant and highly valuable if either (1) it is an “indicator”, which reduces our uncertainty about the value of a parameter in our mental model for making sense of the dynamic macro system, or (2) it is a “surprise” which increases our uncertainty about either the range of potential values for a parameter or the structure of our model.

Each week in this newsletter we review high value new evidence and its significance in some or all of these areas. Each quarter we summarize these weekly newsletters in new issues of The Index Investor and Retired Investor, as well as updated 12 and 36-month global macro regime probabilities and any changes to our model portfolios.

The Neutral portfolio places 10% weights on nine major asset classes, and 5% each to two active strategies (Equity Market Neutral and Global Macro), which should have low correlations with returns on major asset classes.

The Systematic portfolio changes asset class weights based on the extent of our estimate of their respective degrees of over or undervaluation. This portfolio expands the fixed income asset class to include possible allocations to Investment Grade and High Yield credit products. Allocations to Equity Market Neutral and Global Macro remain constant at 5% each. Finally, when some asset classes are so overvalued that they have a zero weight, but other asset classes are not sufficiently undervalued to absorb reallocations away from the overvalued classes, the excess cash is placed in a mix of Cash (short term Treasury Bills and Notes) and Gold.

The Subjective portfolio is our attempt to outperform the Neutral and Systematic portfolios via active management. More often than not, it underperforms the Systematic portfolio, proving that we find successful active management over the long term just as challenging as everyone else.

Model Portfolio Performance

In the second quarter of 2022, as high valuations retreated across multiple asset classes, the Neutral portfolio was down (10.1%) from the end of March, the Systematic portfolio was down (8.1%), and the Subjective portfolio was down (8.0%). By comparison, a Traditional portfolio of 60% US Equity and 40% US Government Bonds was down (11.4%).

For the first half of 2022, the Neutral portfolio was down (8.0%) from 31 December 2021, the Systematic portfolio was down (4.9%), and the Subjective portfolio was down (5.0%). By comparison, a Traditional portfolio of 60% US Equity and 40% US Government Bonds was down (8.7%).