New Global Macro Evidence and Forecasts

New Global Macro Evidence and Forecasts

New Evidence This Week

Health

Since we began to publish The Index Investor in 1997, one of the “wildcard scenarios” we regularly considered in our assessments of emerging risks was a global pandemic caused by a strain of influenza with a high infection fatality rate. Specifically, we have focused on the H5N1 and H7N9 strains of avian influenza. For example, see this pandemic influenza briefing in our May 2009 issue, or this section of the research library on our website.

While there have been scattered cases of human infection (generally people who work on poultry farms), to date neither H5N1 nor H7N9 has become easily transmitted among humans. And that is a very good thing. What has made many medical professionals particularly fearful of H5N1 has been the evidence of its broad tropism, with apparently severe effects on a range of organs, including the brain, liver, and intestinal tract because of its ability to induce much more severe inflammatory reactions than other influenza strains. When people have become infected with H5N1, the fatality rate has been about 60%. In comparison, the highest estimate of the global infection fatality rate for COVID was 2.5%.

This year has seen the emergence of a global H5N1 pandemic – but fortunately among birds, not humans. However, recent developments have substantially increased our concern that H5N1 is mutating in way that increases the probability of a human pandemic. Ten years ago researchers found that only four or five mutations were required for H5N1 to become more easily transmissible among mammals (see, The Potential For Respiratory Droplet Transmissible A/H5N1 Influenza Virus To Evolve In A Mammalian Host, by Russell et al). In June, the New York Times reported evidence of H5N1 in foxes, bobcats, otters, and lynx. A story earlier this month reported that H5N1 infection had been detected in seals in Quebec. We recommend paying much closer attention to new stories about the H5N1 influenza virus in mammals, as well as stories about evolving genetic changes in the virus.

New research has provided more insight about the long-term effects of COVID infection on health. In Neurological And Psychiatric Risk Trajectories After SARS-Cov-2 Infection: An Analysis Of 2-Year Retrospective Cohort Studies Including 1 284 437 Patients, Taquet et al report that “risks of cognitive deficit (known as brain fog), dementia, psychotic disorders, and epilepsy or seizures were still increased at the end of the 2-year follow-up period”, relative to people who were never infected with COVID. The greatest risk, relative to uninfected people, was for cognitive deficit (brain fog). The good news is that infection with the Omicron variant appears to produce much lower rates of these conditions. This study provides further evidence that health care systems and the economy will face increase costs in the future associated with chronic conditions resulting from COVID infection. However, the amount of these costs at this point still remains highly uncertain.

Environment

In The Index Investor and Retired Investor, we have repeatedly highlighted the high degree of complexity in integrated climate models, and the resulting high degree of uncertainty associated with their forecasts. As a result, we still know far too little about the probabilities associated with various climate-driven threats. A new paper approaches this problem from the other direction. In Climate Endgame: Exploring Catastrophic Climate Change Scenarios, Kemp et al provide an overview of “bad to worst case” climate scenarios, and propose an agenda for developing a much better understanding of them.

Technology

Commissioned by the US Department of Homeland Security, RAND’s new analysis, Preparing for Post-Quantum Critical Infrastructure provides high-level assessments of quantum vulnerabilities in 55 national critical functions (NCFs). It finds that, “A significant portion of the vulnerability can be addressed with relatively few actions by the critical enablers.” However, the study also warns that, “many factors related to the cryptographic transition are still uncertain and in need of more-detailed assessment.” This is a critical uncertainty that should not be overlooked in medium and long-term forecasts.

Economy

As we get closer to winter, it still seems as though investors have yet to fully appreciate the scale and possible outcomes of the complex crisis that lies ahead in Europe. On the energy front, with dim prospects for increasing the supply of natural gas to replace Russian pipeline flows, and with governments desperate to avoid a sharp spike in prices, the only alternative is demand reduction. The simplest move would be to convince customers that use gas for space heating to turn down their thermostats. It that doesn’t happen, then there will be cutbacks in supplies to industrial users and electric generators, which will have much larger negative effects on the economy – and via a knock on effect, on social anger, political frustration, and support for continued support for the Ukraine in its war with Russia. So keep your eye on demand side management news from Europe.

The Long Term Budget Outlook from the US Congressional Budget Office makes grim reading. “Rising interest costs and growth in spending on the major health care programs and Social Security—driven by the aging of the population and growth in health care costs per person— boost federal outlays significantly over the 2025–2052 period… Federal deficits over the 2022–2052 period average 7.3 percent of GDP (more than double the average over the past half-century) and generally grow each year, reaching 11.1 percent of GDP in 2052. That projected growth in total deficits is largely driven by increases in interest costs: Net interest outlays more than quadruple over the period, rising to 7.2 percent of GDP in 2052. Primary deficits—that is, deficits excluding net outlays for interest—grow from 2.3 percent of GDP in 2022 to 3.9 percent in 2052…

“In CBO’s projections, debt as a percentage of GDP begins to rise in 2024, surpasses its historical high in 2031 (when it reaches 107 percent), and continues to climb thereafter, rising to 185 percent of GDP in 2052. Debt that is high and rising as a percentage of GDP could slow economic growth, push up interest payments to foreign holders of U.S. debt, heighten the risk of a fiscal crisis, elevate the likelihood of less abrupt adverse effects, make the U.S. fiscal position more vulnerable to an increase in interest rates, and cause lawmakers to feel more constrained in their policy choices.”

While most investors are aware of the policy constraints heavily indebted developing countries face, I think far fewer understand that this can also happen to developed nations too. For example, in May the Banque de France held a conference on “The Sustainability of French Debt, Between Rising Interest Rates and European Rules.” Moreover, the root causes of this problem are deep and complex, and include all the factors that cause low productivity growth, as well as those that block effective political action to address them.

A new McKinsey report (A Reflection On Global Food Security Challenges Amid The War In Ukraine And The Early Impact Of Climate Change) highlights the emerging threat to the global food system. Emerging shortages could “result in a deficit of roughly 15 million to 20 million metric tons of wheat and corn from the world’s supply of exported grain in 2022. The deficit in 2023 could reach roughly 23 million to 40 million metric tons, according to our worst-case scenario… [This] represents a year’s worth of nutritional intake for up to 250 million people, the equivalent of 3 percent of the global population. In addition to the human suffering this implies, based on the experiences of recent food crises, there are a host of other possible destabilizing consequences”, particularly in countries that are heavily dependent on imported grains. For example, in 2021, the world’s largest wheat importers were Indonesia, Nigeria, China, Turkey, and Egypt.

National Security

As we face the second Cold War, a new analysis from AEI’s Mackenzie Eaglen highlights the demographic risks facing the US Military. In Recruitment Is Now a Real Threat to aFrail Force Facing Formidable Foes, she finds that, “Of the 32 million Americans age-eligible for uniformed service, only 23 percent are initially qualified to serve. Once academic eligibility is accounted for, that drops to just over 10 percent (3.53million). But wait, it gets worse! Decades beyond mandatory conscription, the key question now is how many youth are even interested in military service. Only nine percent of eligible young people in the US demonstrated the propensity to serve, according to the survey data, leaving around 321,000 — a brutally low 1.01 percent — of the total age-eligible population both qualified and inclined to join the military.”

In Playing with Fire in the Ukraine, John Mearsheimer observes that, “The threat to Russia today is even greater than it was before the war, mainly because the Biden administration is now determined to roll back Russia’s territorial gains and permanently cripple Russian power. Making matters even worse for Moscow, Finland and Sweden are joining NATO, and Ukraine is better armed and more closely allied with the West. Moscow cannot afford to lose in Ukraine, and it will use every means available to avoid defeat…

“In essence, Kyiv, Washington, and Moscow are all deeply committed to winning at the expense of their adversary, which leaves little room for compromise. Neither Ukraine nor the United States, for example, is likely to accept a neutral Ukraine; in fact, Ukraine is becoming more closely tied with the West by the day. Nor is Russia likely to return all or even most of the territory it has taken from Ukraine, especially since the animosities that have fueled the conflict in the Donbas between pro-Russian separatists and the Ukrainian government for the past eight years are more intense than ever. These conflicting interests explain why so many observers believe that a negotiated settlement will not happen any time soon and thus foresee a bloody stalemate. They are right about that. But observers are underestimating the potential for catastrophic escalation that is built into a protracted war in Ukraine.”

US Seventh Fleet Commander Vice Admiral Karl Thomas said China’s decision to fire missiles over Taiwan “must be contested” to prevent such action becoming the new norm. “Contesting” these overflights obviously carries with it the possibility of further escalation of the intensifying conflict between China and the United States over Taiwan.

Reading Mearsheimer’s column and Admiral Thomas’s statement, I was reminded once again of the key lesson from a 1983 CIA study of failed forecasts: "Each involved historical discontinuity, and, in the early stages…unlikely outcomes. The basic problem was…situations in which trend continuity and precedent were of marginal, if not counterproductive value."

Investor Behavior and Decision Making

In Human Error In Complex Problem Solving And Dynamic Decision Making: A Taxonomy Of 24 Errors And A Theory, the legendary Dietrich Dorner provides and outstanding overview of this critical issue. It is well-worth a read.

In Overreaction and Diagnostic Expectations in Macroeconomics, Bordalo et al find that, “belief overreaction can account for many long-standing empirical puzzles in macro and finance, which emphasize the extreme volatility and boom-bust dynamics of key time series, such as stock prices, credit, and investment.”

And in a related paper, Sharot et al explore Why and When Beliefs Change. Their research finds that, “the utility of a belief is derived from the potential outcomes of holding it. Outcomes can be internal (e.g., positive/negative feelings) or external (e.g., material gain/loss), and only some are dependent on belief accuracy. Belief change can then be understood as an economic transaction, in which the multidimensional utility of the old belief is compared against that of the new belief. Change will occur when potential outcomes alter across attributes, for example due to changing environments, or when certain outcomes are made more or less salient.” In sum, pure rational analysis and marshaling of evidence and logic is sometimes not sufficient to change beliefs – hence the existence (and impact) of overreaction and excessive extrapolation by investors.

You can improve your own ability to anticipate, accurately assess, and adapt in time to emerging threats by taking our 11 module course at The Strategic Risk Institute. It costs only $250, and leads to a certificate in Strategic Risk Management and Governance.

Background

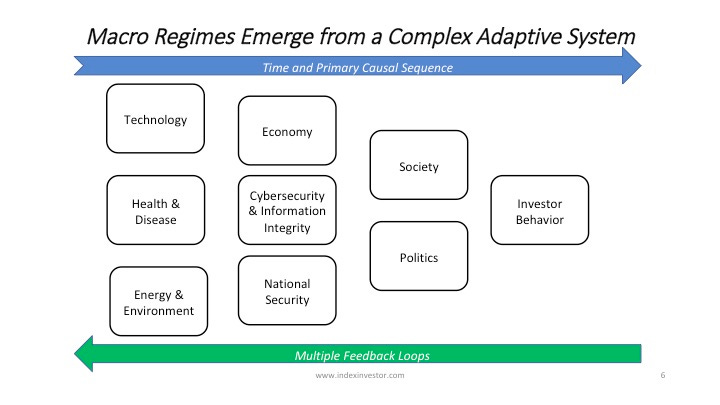

At the Index Investor and Retired Investor, our information collection, analysis, and forecasting process is based on this model of how developments in different issue areas interact in a rough chronological sequence (albeit in a complex manner) to produce different global macro regimes (which we label Normal Times, High Uncertainty, High Inflation, and Persistent Deflation).

In each of these areas we continuously seek new evidence, which classify as significant and highly valuable if either (1) it is an “indicator”, which reduces our uncertainty about the value of a parameter in our mental model for making sense of the dynamic macro system, or (2) it is a “surprise” which increases our uncertainty about either the range of potential values for a parameter or the structure of our model.

Each week in this newsletter we review high value new evidence and its significance in some or all of these areas. Each quarter we summarize these weekly newsletters in new issues of The Index Investor and Retired Investor, as well as updated 12 and 36-month global macro regime probabilities and any changes to our model portfolios.

The Neutral portfolio places 10% weights on nine major asset classes, and 5% each to two active strategies (Equity Market Neutral and Global Macro), which should have low correlations with returns on major asset classes.

The Systematic portfolio changes asset class weights based on the extent of our estimate of their respective degrees of over or undervaluation. This portfolio expands the fixed income asset class to include possible allocations to Investment Grade and High Yield credit products. Allocations to Equity Market Neutral and Global Macro remain constant at 5% each. Finally, when some asset classes are so overvalued that they have a zero weight, but other asset classes are not sufficiently undervalued to absorb reallocations away from the overvalued classes, the excess cash is placed in a mix of Cash (short term Treasury Bills and Notes) and Gold.

The Subjective portfolio is our attempt to outperform the Neutral and Systematic portfolios via active management. More often than not, it underperforms the Systematic portfolio, proving that we find successful active management over the long term just as challenging as everyone else.

Model Portfolio Performance

In the second quarter of 2022, as high valuations retreated across multiple asset classes, the Neutral portfolio was down (10.1%) from the end of March, the Systematic portfolio was down (8.1%), and the Subjective portfolio was down (8.0%). By comparison, a Traditional portfolio of 60% US Equity and 40% US Government Bonds was down (11.4%).

For the first half of 2022, the Neutral portfolio was down (8.0%) from 31 December 2021, the Systematic portfolio was down (4.9%), and the Subjective portfolio was down (5.0%). By comparison, a Traditional portfolio of 60% US Equity and 40% US Government Bonds was down (8.7%).