New Macro Evidence and Forecast Updates

New Macro Evidence and Forecast Updates

“We underrate the unpredictability of the future because we overrate the inevitability of the past” — Marc Andreessen

New Evidence This Week

Technology

In Emergent Abilities of Large Language Models, Jason Wei and his fellow authors from Google, Stanford, UNC Chapel Hill, and Deep Mind write that, “In recent years, a new paradigm has evolved around language models — neural networks that simply predict the next words in a sentence given the prior words in the sentence. After being trained on a large unlabeled corpus of text using this objective, language models can be "prompted" to perform arbitrary tasks framed as next word prediction…

“This new paradigm represents a shift from task-specific models, trained to do a single task, to task-general models, which can perform many tasks. Task-general models can even perform new tasks that were not explicitly included in their training data. For instance, GPT-3 showed that language models could successfully multiply two-digit numbers, even though they were not explicitly trained to do so. However, this ability to perform new tasks only occurred for models that had a certain number of parameters and were trained on a large-enough dataset.

“The idea that quantitative changes in a system (e.g., scaling up language models) can result in new behavior is known as emergence, which has been observed in complex systems across many disciplines such as physics, biology, economics, and computer science.” In the case of large language models, their definition is that “an ability is emergent if it is not present in smaller models but is present in larger models.” After noting the increase in emergent capabilities that has occurred as language models have grown in scale, the authors note that further scaling will also lead not only to continuing emergence, not just of new capabilities, but also new risks, many of which are difficult to foresee (e.g., those that arise from the interaction of new model capabilities and the models’ use in a widening range of applications). For more on such risks, see also Predictability and Surprise in Large Generative Models, by Ganguli et al.

The “Special Competitive Studies Project” “is a bipartisan, non-profit initiative with a clear mission: to make recommendations to strengthen America’s long-term competitiveness for a future where artificial intelligence (AI) and other emerging technologies reshape America’s national security, economy, and society.” In America Could Lose the Tech Contest with China, two members of the project, Eric Schmidt and Yll Bajraktari, summarize the findings of SCSP’s new report, Mid-Decade Challenges to National Competitiveness.

The authors note that, “technology is at the heart of the U.S.-Chinese competition to build a thriving society, a growing economy, and sharper instruments of power. At stake is the future of political freedom, open markets, democratic government, and a world order rooted in democratic values and cooperation rather than authoritarianism and coercion. Washington needs a national plan that brings together commercial, academic, and government sectors to carry out a techno-industrial strategy…

“As Washington has fiddled, Beijing’s centralized system for high-tech research and development has churned, investing billions of dollars, training students, and subsidizing tech companies. It is entirely possible to imagine a future where systems designed, built, and based in China dominate world markets, extending Beijing’s sphere of influence and providing it with a military advantage over the United States”…

“The to-do list [facing the United States] is admittedly long and daunting. But technological competition with China will only intensify in the years to come. And in this contest, there will be almost no margin for error. Action on all fronts must start now.”

Health and Disease

A dolphin in Florida and a porpoise in Sweden were found to be infected with H5N1 influenza, providing further evidence that the current global avian H5N1 pandemic has genetic mutations and reassortments that are enabling the spread to mammals. Given the very high infection fatality rate of H5N1 infections in humans (see our previous posts on this issue), this continues to be an emerging threat that warrants careful monitoring.

Newly published research (Imprinted SARS-Cov-2 Humoral Immunity Induces Convergent Omicron RBD Evolution and Omicron Sublineage BA.2.75.2 Exhibits Extensive Escape From Neutralising Antibodies) has found that the BA.2.75.2 strain of the SARS-CoV-2 virus is very effective at evading immunity conferred by vaccination and/or previous COVID infections. The good news is that while BA.2.75.2 has spread rapidly in India, it has not yet led to a surge in either hospitalizations or deaths.

The Lancet Commission on Lessons for the Future from the COVID Pandemic has published its report. The extensive list of failures it catalogues makes for sobering reading in light of the pre-COVID claims made by many governments and international organizations about how well prepared they were for the global respiratory disease pandemic they knew would one day arrive.

Economy

In their new paper, Inflation as a Fiscal Limit, Bianchi and Melosi focus on the likely persistence of current inflationary pressures. “Will inflation fall as rapidly as it rose, following a similar pattern observed after the Second World War and the Korean War in the United States? Or will inflation drift up as observed in the late 1960s and 1970s in many advanced economies?” They argue that, “the answer to these important questions hinges predominantly on the fiscal authority’s credibility in stabilizing a large fiscal imbalance. The central bank’s anti-inflation reputation, albeit important, is not decisive. Trend inflation is fully controlled by the monetary authority only when public debt can be successfully stabilized by credible future fiscal plans. When the fiscal authority is not perceived as fully responsible for covering the existing fiscal imbalances [via higher taxes and/or lower spending], the private sector expects that inflation will rise to ensure sustainability of [the growing] national debt. As a result, a large fiscal imbalance combined with a weakening fiscal credibility may lead trend inflation to [rise above] the long-run target chosen by the monetary authority.”

In other words, the result will be stagflation. Unless, of course, there is sufficient public and private investment, in new physical, digital, and human capital, to substantially increase productivity and the growth rate of the economy. However, as Oren Cass vividly showed in his excellent analysis (The Rise of Wall Street and the Fall of American Investment) this has clearly not been happening in recent years. Perhaps the new Cold War and the need to increase supply chain resiliency and reshore production will change this. But until we see clear evidence that this is the case, stagflation will remain an emerging threat.

Russia has cut off natural gas flows to Western Europe, which has sharply increased energy prices – even before the start of heating season really drives up demand. Moreover, this problem isn’t limited to Europe. It has also driven up natural gas prices in the United States, which is going to have a big impact on electricity costs and heating bills in the United States too. What remains to be seen is the impact this will have on aggregate demand, bankruptcies, and debt market. If the impacts are severe, second and third order effects will very likely be non-linear. Put simply, there is probably a lot more downside risk than many currently realize (for example, see this new IMF analysis, on The Systemic Impact of Debt Default in a Multilayered Global Network Model).

Federal Reserve economist Michael Smolyansky published an important new FEDS Note titled, The Coming Long-Run Slowdown in Corporate Profit Growth and Stock Returns. His analysis concludes that, “Over the past two decades, the corporate profits of stock market listed firms have been substantially boosted by declining interest rate expenses and lower corporate tax rates. This note's key finding is that the reduction in interest and tax expenses is responsible for a full one-third of all profit growth for S&P 500 nonfinancial firms over the prior two-decade period. I argue that the boost to corporate profits from lower interest and tax expenses is unlikely to continue, indicating notably lower profit growth, and thus stock returns, in the future.”

In New Frontiers: The Origins and Content of New Work, 1940-2018, David Autor and his fellow authors continue his ongoing exploration on the labor market impacts of rapidly improving cognitive and physical automation technologies. In their framework, such technologies can either substitute for human labor, or complement (augment) it. This paper concludes that, “the [labor] demand-eroding effects of automation innovations have intensified in the last four decades while the [labor] demand-increasing effects of augmentation innovations have not.” In turn, this has accelerated the polarization of the labor market and the disappearance of middle skill jobs, with clear implications for future social anger and political conflict.

National Security

Ukrainian troops have achieved major victories against the Russian army, and regained over 3,000 square kilometers of occupied territory. In response, President Putin has called up 300,000 Russian Army reservists. However, as most of them are previous conscripts who received poor training, and as Russia’s stocks of modern equipment have been badly depleted, they are very unlikely to significantly change the situation on the ground in Ukraine anytime soon. Clearly, Putin knows this, and that Russia’s situation in the Ukraine has badly worsened. This almost certainly was the motivation behind his renewed threat to “use all available means” (code for nuclear weapons) to “defend Russian territory” (which in Putin’s mind seems to include the Ukraine).

Russia’s willingness to use nuclear weapons if the situation in the Ukraine continues to worsen remains a critical uncertainty. Two of the best recent analyses of it are Chatham House’s Myths and Misconceptions Around Russian Military Intent, and Escalation Management And Nuclear Employment In Russian Military Strategy, by Kofman and Fink. Critically, the latter observe that, “The challenge posed by Russian nuclear strategy is not just a capability gap, but a cognitive gap. The Russian military establishment has spent decades thinking and arguing about escalation management, the role of conventional and nuclear weapons, targeting, damage, etc. In the United States, precious little attention has been paid to the question of escalation management, which is overshadowed by planning for warfighting…There is an implicit assumption in U.S. defense strategy that Washington can somehow control escalation and dissuade nuclear use on the part of others, without any discernible plan for accomplishing this feat.”

Once again, President Biden stated that the United States would defend Taiwan if it was attacked by China, and once again his staff tried to walk it back.

AEI’s Hal Brands published a column provocatively titled, Ukraine War Shows the US MilitaryIsn’t Ready for War With China. He began by noting the seriousness of the situation we face. The threat that China will attack Taiwan “isn’t some well-kept secret: National Security Adviser Jake Sullivan recently told Bloomberg News that there is a “distinct threat” of a Chinese invasion of Taiwan. Director of National Intelligence Avril Haines has characterized that threat as “acute.” In public, the Pentagon now says only that it does not expect an invasion in the next two years. The impression one gets from conversations around Washington is that many officials believe that a major Chinese use of force against Taiwan — whether an outright invasion or simply a coercive blockade — could come in the next three to five years, once President Xi Jinping is more confident that his fast-modernizing People’s Liberation Army can prevail…

“Whether the US is ready for the train wreck that so many of its own officials see coming is a different matter… Modern war is prodigiously costly: It destroys some of the most exquisite, expensive creations modern societies can produce. It consumes epic quantities of missiles, artillery shells and other munitions; it can wreck hard-to-replace planes, tanks and warships in large numbers. The Ukraine war is a case study in how hard it can be simply to keep fighting in high-intensity conflict: A free-world coalition led by a global superpower has struggled to meet the Kyiv government’s needs without dangerously depleting its own stockpiles…The US needs to take a vital lesson from the war in Ukraine — as well as from its own experience, generations ago, in World War II. If America wants to win a potential great-power war with China a few years from now, it had better start rearming far more seriously before the shooting starts.”

In sum, the emerging threats of potential Russian use of a nuclear weapon, a potential Chinese attack on Taiwan, and the threat that the United States would not prevail (or would prevail at an extremely high price) if it defends Taiwan add up to a degree of uncertainty and potential danger the world has not seen in decades. And most people still seem unaware of the situation we face.

In America’s Education Crisis Is a National Security Threat Eberstadt and Abramsky state that, “Education is a crucial component of human capital and, by extension, of national might. A better-educated citizenry means a more productive economy and thus greater military potential. But because the educational explosion of the last 70 years has been uneven—some countries have made greater strides than others, and the pace of progress has varied over time—this dramatic transformation hasn’t just increased the overall size of the global economy. It has also shifted the distribution of economic potential among countries, including great powers.”

However, “comparatively speaking, Western nations, including the United States, have been the biggest losers in this great reshuffling of educational and economic heft…Whether the United States can weather these changes without forfeiting its position of economic and military dominance will depend in part on its ability to recognize and address the ominous stagnation in its classrooms.”

Society

Pew Research’s new study, Modeling the Future of Religion in America, reported that, “Since the 1990s, large numbers of Americans have left Christianity to join the growing ranks of U.S. adults who describe their religious identity as atheist, agnostic or “nothing in particular.” This accelerating trend is reshaping the U.S. religious landscape.” Pew estimates “that in 2020, about 64% of Americans, including children, were Christian. People who are religiously unaffiliated, sometimes called religious “nones,” accounted for 30% of the U.S. population. Adherents of all other religions – including Jews, Muslims, Hindus and Buddhists – totaled about 6%.

“Depending on whether religious switching continues at recent rates, speeds up or stops entirely, the projections show Christians of all ages shrinking from 64% to between a little more than half (54%) and just above one-third (35%) of all Americans by 2070. Over that same period, “nones” would rise from the current 30% to somewhere between 34% and 52% of the U.S. population…The decline of Christianity and the rise of the “nones” may have complex causes and far-reaching consequences for politics, family life and civil society.”

You can improve your own ability to anticipate, accurately assess, and adapt in time to emerging threats by taking our 11 module course at The Strategic Risk Institute. It costs only $250, and leads to a certificate in Strategic Risk Management and Governance.

Background

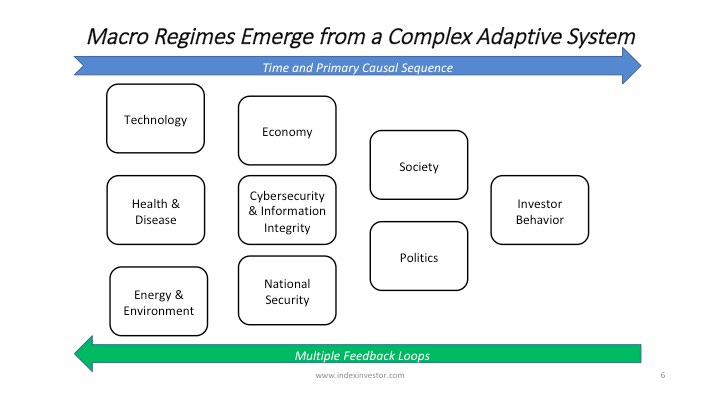

At the Index Investor and Retired Investor, our information collection, analysis, and forecasting process is based on this model of how developments in different issue areas interact in a rough chronological sequence (albeit in a complex manner) to produce different global macro regimes (which we label Normal Times, High Uncertainty, High Inflation, and Persistent Deflation).

In each of these areas we continuously seek new evidence, which classify as significant and highly valuable if either (1) it is an “indicator”, which reduces our uncertainty about the value of a parameter in our mental model for making sense of the dynamic macro system, or (2) it is a “surprise” which increases our uncertainty about either the range of potential values for a parameter or the structure of our model.

Each week in this newsletter we review high value new evidence and its significance in some or all of these areas. Each quarter we summarize these weekly newsletters in new issues of The Index Investor and Retired Investor, as well as updated 12 and 36-month global macro regime probabilities and any changes to our model portfolios.

The Neutral portfolio places 10% weights on nine major asset classes, and 5% each to two active strategies (Equity Market Neutral and Global Macro), which should have low correlations with returns on major asset classes.

The Systematic portfolio changes asset class weights based on the extent of our estimate of their respective degrees of over or undervaluation. This portfolio expands the fixed income asset class to include possible allocations to Investment Grade and High Yield credit products. Allocations to Equity Market Neutral and Global Macro remain constant at 5% each. Finally, when some asset classes are so overvalued that they have a zero weight, but other asset classes are not sufficiently undervalued to absorb reallocations away from the overvalued classes, the excess cash is placed in a mix of Cash (short term Treasury Bills and Notes) and Gold.

The Subjective portfolio is our attempt to outperform the Neutral and Systematic portfolios via active management. More often than not, it underperforms the Systematic portfolio, proving that we find successful active management over the long term just as challenging as everyone else.

Model Portfolio Performance

In the second quarter of 2022, as high valuations retreated across multiple asset classes, the Neutral portfolio was down (10.1%) from the end of March, the Systematic portfolio was down (8.1%), and the Subjective portfolio was down (8.0%). By comparison, a Traditional portfolio of 60% US Equity and 40% US Government Bonds was down (11.4%).

For the first half of 2022, the Neutral portfolio was down (8.0%) from 31 December 2021, the Systematic portfolio was down (4.9%), and the Subjective portfolio was down (5.0%). By comparison, a Traditional portfolio of 60% US Equity and 40% US Government Bonds was down (8.7%).